EPF ‘VE’ Strategy: How an Extra 2% Contribution Can Significantly Grow Your Retirement Savings

KUALA LUMPUR, Oct 1 — Many people struggle to save more for retirement, often spending what they could set aside. A practical solution is to let savings be deducted automatically through the Employees Provident Fund (EPF).

KUALA LUMPUR, Oct 1 — Many people struggle to save more for retirement, often spending what they could set aside. A practical solution is to let savings be deducted automatically through the Employees Provident Fund (EPF).

This is where EPF’s Voluntary Excess (VE) scheme comes in, allowing employees to contribute more than the mandatory 11 per cent of their salary into retirement savings.

Voluntary Excess (VE)

By law, employees contribute 11 per cent of their salary, while employers add 12 or 13 per cent depending on income level. With VE, employees can voluntarily contribute above 11 per cent.

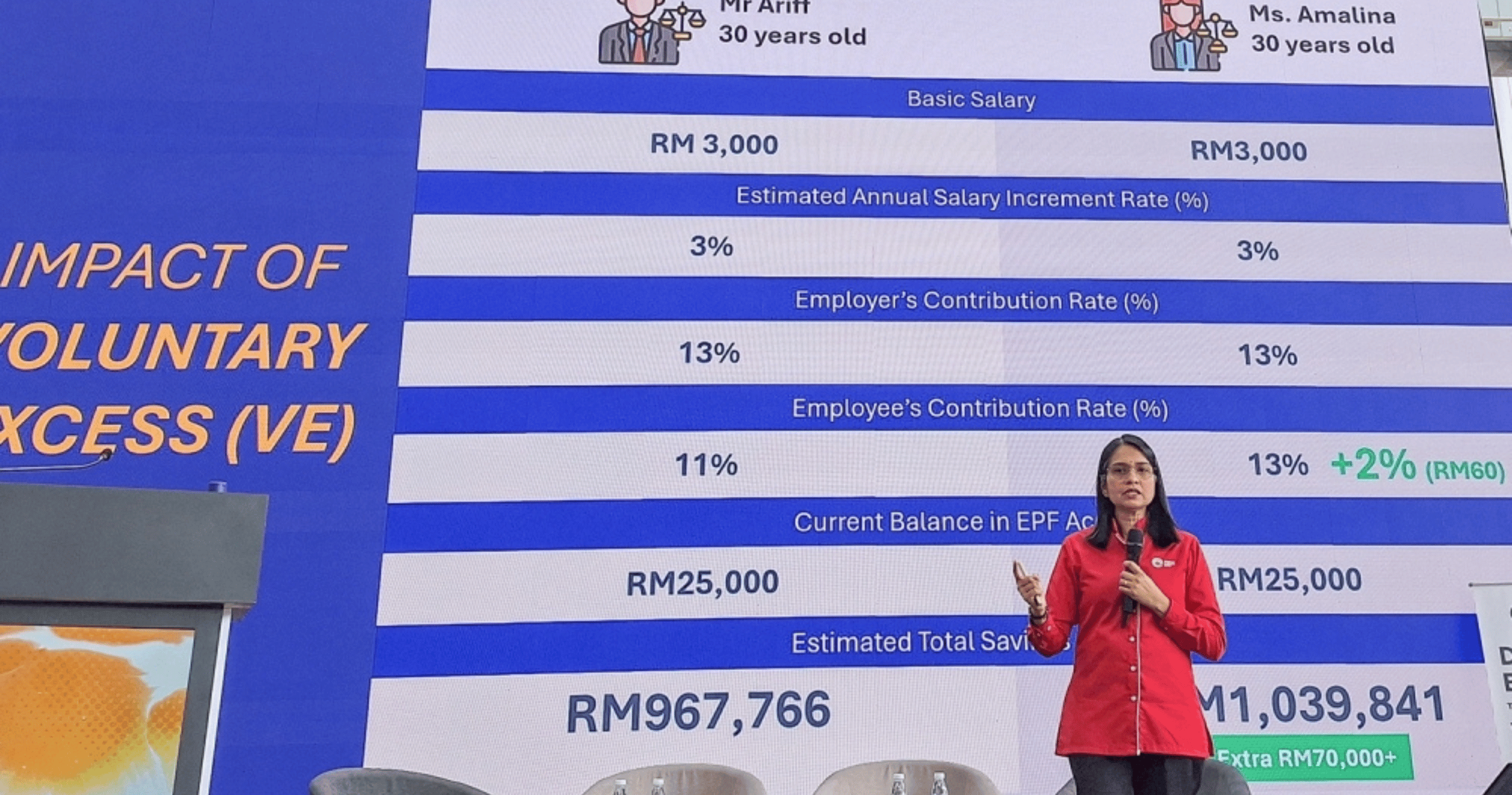

EPF adviser Mogana Murugan @ Arujunan highlighted how even a small increase makes a big difference. For example, raising contributions to 13 per cent (just 2 per cent more) can significantly grow retirement savings.

She illustrated this with two 30-year-olds, both earning RM3,000 monthly with 3 per cent annual salary increments and RM25,000 in EPF savings.

11% contribution: Estimated RM967,000 at age 60.

13% contribution: Estimated RM1,039,000 at age 60 — about RM70,000 more.

This assumes no withdrawals and a 5 per cent annual dividend. The difference begins with just RM60 extra a month and grows steadily with salary increments.

How to contribute through VE

There is no maximum limit for VE contributions. Some members even contribute 40 per cent of their salary. To apply, download the form from the EPF website and submit it to your employer.

Self-Contribution Option

Another method is voluntary top-ups, allowing up to RM100,000 a year through the i-Akaun app. This option gives flexibility to decide when and how much to contribute.

Steps:

Log in to i-Akaun → “Increase savings: Top-up now.”

Skip i-Saraan registration (for self-employed).

Enter the desired amount under “self” and transfer from your bank.

The “Auto Tambah” function, currently available for RHB and AmBank, allows automatic monthly deductions from your bank account.

VE vs Self-Contribution

VE: Automatic monthly salary deduction, disciplined and consistent.

Self-Contribution: Flexible, requires manual action but allows larger sums.

Retirement needs

EPF contributions can begin at age 14 and continue until 75, with dividends paid up to age 100. The required amount for retirement depends on lifestyle and inflation, but even small extra contributions can create significant long-term benefits.

At the Malaysian Bar’s MyBar Carnival 2025, EPF’s Relationship & Advisory (RA) adviser Mogana Murugan shows how even saving two per cent more from your salary can make a big impact on your EPF retirement savings. — Picture by Ida Lim

BANGKOK, April 24 — Thailand’s Supreme Court on Friday agreed to hear a petition accusing 44 current and former opposition lawmakers of ethics violations over their 2021 move to amend a law protecting the monarchy from criticism, according to Thai media reports.

PUTRAJAYA, April 24 — The Court of Appeal today dismissed Kepala Batas MP Dr Siti Mastura’s appeal against a High Court ruling ordering her to pay RM825,000 in damages and costs for defaming three DAP leaders by linking them to former Communist Party of Malaya leader Chin Peng.

THE HAGUE, April 23 — Former Philippines president Rodrigo Duterte will stand trial at the International Criminal Court after judges on Thursday confirmed charges of crimes against humanity over his controversial “war on drugs.”